[ Mon, Feb 02nd ]: Investopedia

[ Mon, Feb 02nd ]: NBC 7 San Diego

[ Mon, Feb 02nd ]: dpa international

[ Mon, Feb 02nd ]: South Bend Tribune

[ Mon, Feb 02nd ]: MDM

[ Mon, Feb 02nd ]: Los Angeles Times

[ Mon, Feb 02nd ]: BBC

[ Mon, Feb 02nd ]: reuters.com

[ Mon, Feb 02nd ]: The New Indian Express

[ Mon, Feb 02nd ]: U.S. News & World Report

[ Mon, Feb 02nd ]: Wyoming News

[ Mon, Feb 02nd ]: Semafor

[ Mon, Feb 02nd ]: Seattle Times

[ Mon, Feb 02nd ]: The West Australian

[ Mon, Feb 02nd ]: People

[ Mon, Feb 02nd ]: Billboard

[ Mon, Feb 02nd ]: News 12 Networks

[ Mon, Feb 02nd ]: KOB 4

[ Mon, Feb 02nd ]: legit

[ Mon, Feb 02nd ]: The New Zealand Herald

[ Mon, Feb 02nd ]: Patch

[ Mon, Feb 02nd ]: TMJ4

[ Mon, Feb 02nd ]: The Gazette

[ Mon, Feb 02nd ]: Killeen Daily Herald

[ Mon, Feb 02nd ]: Channel NewsAsia Singapore

[ Mon, Feb 02nd ]: KTBS

[ Mon, Feb 02nd ]: ThePrint

[ Sun, Feb 01st ]: NBC News

[ Sun, Feb 01st ]: The New Zealand Herald

[ Sun, Feb 01st ]: Cleveland.com

[ Sun, Feb 01st ]: Investopedia

[ Sun, Feb 01st ]: The Independent

[ Sun, Feb 01st ]: The Hill

[ Sun, Feb 01st ]: Toronto Star

[ Sun, Feb 01st ]: The Center Square

[ Sun, Feb 01st ]: Fox News

[ Sun, Feb 01st ]: The Boston Globe

[ Sun, Feb 01st ]: World Socialist Web Site

[ Sun, Feb 01st ]: Seattle Times

[ Sun, Feb 01st ]: WTOP News

[ Sun, Feb 01st ]: kcra.com

[ Sun, Feb 01st ]: CBS News

[ Sun, Feb 01st ]: Politico

[ Sun, Feb 01st ]: BBC

[ Sun, Feb 01st ]: The New Indian Express

[ Sun, Feb 01st ]: Telangana Today

[ Sun, Feb 01st ]: NDTV

[ Sun, Feb 01st ]: CNN

Goods vs. Services: Inflation's Uneven Path

Investopedia

InvestopediaLocale: UNITED STATES

A Tale of Two Inflation Drivers: Goods vs. Services

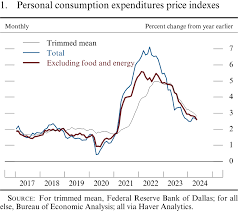

The latest PCE data reveals a familiar dynamic: a continued deceleration in goods inflation coupled with stubbornly high services inflation. This divergence is central to the Fed's current predicament. Goods prices, susceptible to supply chain adjustments and shifts in demand, have shown a welcome easing in recent months. Durable goods inflation, encompassing items like vehicles, saw a modest increase of 0.1% in November, following a 0.2% rise in October. Non-durable goods, including clothing and food, remained largely stable.

However, the same can't be said for the services sector. Services inflation is proving far more resistant to the Fed's tightening efforts. This is due to the fundamentally different nature of service provision. Unlike goods, services are often labor-intensive and tied to factors like wages, rents, and other contractual obligations. These components are less flexible and respond more slowly to monetary policy interventions. In November, the shelter component - a key measure of housing costs - rose by 0.3%, continuing to be a significant driver of overall inflation. This rise in shelter costs reflects both current rental prices and owners' equivalent rent, which is often a lagging indicator of housing market trends.

Decoding the Fed's Response: Hawkish Stance Expected to Continue

The implication of these numbers is clear: the Federal Reserve is likely to maintain its hawkish monetary policy stance for the foreseeable future. "Core inflation is decelerating, but not rapidly," observed Veronica Catanaro, senior investment strategist at Firstrust Bank, accurately summarizing the prevailing sentiment amongst economists. This suggests that while the Fed may not necessarily accelerate the pace of rate hikes, it's unlikely to pivot to a more dovish position anytime soon.

The market currently anticipates just one further rate hike before the end of the year, but even this single increase is viewed with caution. Analysts believe the market might be able to absorb one more hike, but any further tightening beyond that could significantly increase the risk of a recession. The Fed is walking a tightrope - attempting to curb inflation without triggering a severe economic downturn.

Looking Ahead: What Must Change for a Policy Shift?

The key question now is what would prompt the Fed to alter its course? A sustained and significant deceleration in services inflation is the most crucial factor. The Fed will be meticulously monitoring indicators such as wage growth, rental trends, and the demand for various services. A consistent downward trend in these areas would provide the confidence needed to signal a potential shift in policy.

Furthermore, the Fed will be closely watching other economic data, including employment figures, consumer spending, and global economic conditions. A weakening labor market or a slowdown in consumer demand could also influence the Fed's decisions. However, given the current resilience of the economy, the bar for a policy pivot remains high.

For consumers and businesses, this means that higher interest rates are likely to persist for a considerable period, impacting borrowing costs for mortgages, auto loans, and corporate investments. While the slowdown in goods inflation offers some relief, the stickiness of services inflation suggests that the fight against rising prices is far from over. The Fed's commitment to its 2% inflation target, combined with the latest PCE data, points to a prolonged period of monetary tightening and ongoing economic uncertainty.

Read the Full Investopedia Article at:

[ https://www.investopedia.com/the-fed-s-favorite-inflation-measure-stayed-hot-in-november-11890434 ]

[ Sat, Jan 31st ]: NPR

[ Fri, Jan 30th ]: Investopedia

[ Fri, Jan 30th ]: People

[ Wed, Jan 14th ]: WBAY

[ Tue, Dec 30th 2025 ]: The Globe and Mail

[ Sun, Dec 21st 2025 ]: The New Indian Express

[ Mon, Dec 01st 2025 ]: The Globe and Mail

[ Wed, Nov 26th 2025 ]: The Associated Press

[ Sat, Oct 04th 2025 ]: Seeking Alpha

[ Tue, Dec 17th 2024 ]: The Financial Times

[ Thu, Dec 12th 2024 ]: The Financial Times

[ Tue, Dec 10th 2024 ]: The New York Times